Black-Scholes model of option pricing

Consider a public company with stock price  at time

at time  . A European style option on the stock of this company is a contract to have the option to buy the stock at a predetermined price on a predetermined future time. The option is described by the strike price

. A European style option on the stock of this company is a contract to have the option to buy the stock at a predetermined price on a predetermined future time. The option is described by the strike price  , the strike time and its price

, the strike time and its price  . Paying to buy an option gives us the opportunity to buy the stock for the strike price at the strike time . At time , the worth of the option depends on the value of the stock . If the stock has fallen below the strike price , i.e., if

. Paying to buy an option gives us the opportunity to buy the stock for the strike price at the strike time . At time , the worth of the option depends on the value of the stock . If the stock has fallen below the strike price , i.e., if  the option becomes worthless because it is more convenient to pay the actual price for the stock and forgo the option. If, on the contrary, the price has risen beyond , i.e., if

the option becomes worthless because it is more convenient to pay the actual price for the stock and forgo the option. If, on the contrary, the price has risen beyond , i.e., if  we can realize a gain

we can realize a gain  by exercising the option to buy the stock at price . This gain can be cashed immediately by reselling the stock at the current price . We can thus write the worth

by exercising the option to buy the stock at price . This gain can be cashed immediately by reselling the stock at the current price . We can thus write the worth  of the option as

of the option as

![\[w = \big[X(t) - K\big]^{+},\]](https://ese3030.seas.upenn.edu/wp-content/ql-cache/quicklatex.com-534f5abaaf7982dd2daa70a3889ce3e8_l3.png "Rendered by QuickLaTeX.com")

where  denotes projection on the positive numbers.

denotes projection on the positive numbers.

The gain to be realized by the trading strategy “buy option at time  , exercise the option at time if , sell stock at price ” depends on the difference between and . It is not exactly the difference because it is not equivalent to own at time

, exercise the option at time if , sell stock at price ” depends on the difference between and . It is not exactly the difference because it is not equivalent to own at time  and at time . In particular, while the proposed investment strategy incurs some risk of loosing the initial investment , it is possible to invest in a risk-free money market account. If the interest in the money market account is

and at time . In particular, while the proposed investment strategy incurs some risk of loosing the initial investment , it is possible to invest in a risk-free money market account. If the interest in the money market account is  continuously compounded, the worth of the money market investment at time is

continuously compounded, the worth of the money market investment at time is  . Consequently, when comparing investment and payoff it is fairer to compare with because growing to is literally effortless. Equivalently, we can compare to

. Consequently, when comparing investment and payoff it is fairer to compare with because growing to is literally effortless. Equivalently, we can compare to  because capital at time can be grown to at time through a risk-free money market investment. The latter comparison is the one commonly used and, in general, we say that a capital at time has a present value or a time-zero value of . We may also refer to as the discounted worth. Using the option’s worth expression, we can compute the discounted gain of an option investment as

because capital at time can be grown to at time through a risk-free money market investment. The latter comparison is the one commonly used and, in general, we say that a capital at time has a present value or a time-zero value of . We may also refer to as the discounted worth. Using the option’s worth expression, we can compute the discounted gain of an option investment as

![\[w = e^{-\alpha t}\big[X(t)-K\big]^{+} - c .\]](https://ese3030.seas.upenn.edu/wp-content/ql-cache/quicklatex.com-cab0c9bc74caa2c48ab253944ea1207b_l3.png "Rendered by QuickLaTeX.com")

The relevant question here is what is a fair price for an option with strike price to be exercised at time . The answer to this question is given by the Black-Scholes formula for option pricing that uses expectations on the future behavior of the stock to determine the option’s price . To understand Black-Scholes formula, we need to introduce the Geometric Brownian motion model of stock prices, discuss the concept of arbitrages, and define risk neutral measures. The geometric Brownian motion model of stock prices is presented next. For arbitrages and the risk neutral measure you’ll have to wait for the class.

Geometric Brownian motion model of stock prices

It suffices to examine a graph with the evolution of a stock price, e.g., Fig. 1, to realize that stock prices are, to some extent, random. To construct a stochastic model of stock prices, notice that variations in a stock price are likely to be proportional to the price of the stock . That is, if the price of the stock is  , a variation of plus or minus

, a variation of plus or minus  is akin to a variation of plus or minus

is akin to a variation of plus or minus  , when the price is

, when the price is  . A particular class of stochastic processes with such property is geometric Brownian motion (GBM). This model presupposes that relative variations on the price can be described as a Brownian motion with drift. Specifically, it assumes that changes in prices are according to the expression

. A particular class of stochastic processes with such property is geometric Brownian motion (GBM). This model presupposes that relative variations on the price can be described as a Brownian motion with drift. Specifically, it assumes that changes in prices are according to the expression

![\[X(t+s) = X(t) e^{Y_{t}(s)}\]](https://ese3030.seas.upenn.edu/wp-content/ql-cache/quicklatex.com-f1f25815c14b99660504331e445a272d_l3.png "Rendered by QuickLaTeX.com")

where  is normally distributed with mean

is normally distributed with mean  and variance

and variance  independently of

independently of  . Definition of a GBM also requires relative price changes

. Definition of a GBM also requires relative price changes  and

and  in disjoint time intervals to be independent. In the context of stock pricing, the mean

in disjoint time intervals to be independent. In the context of stock pricing, the mean  represents the stock’s drift and the variance

represents the stock’s drift and the variance  its volatility.

its volatility.

An equivalent characterization of a GBM is to state that a process is a GBM if its logarithm  is a regular Brownian motion (BM) with drift. Indeed, taking logarithms in both sides of the previous equation yields

is a regular Brownian motion (BM) with drift. Indeed, taking logarithms in both sides of the previous equation yields

![\[\log X(t+s) = \log X(t) + Y_{t}(s)\]](https://ese3030.seas.upenn.edu/wp-content/ql-cache/quicklatex.com-b79b6ceac0eceb946c0faab43005547b_l3.png "Rendered by QuickLaTeX.com")

The two conditions imposed on , namely that is normal with mean and variance and that and are independent for disjoint time intervals, along with the relationship just derived imply by definition that  is a BM.

is a BM.

An important observation to make here is to consider a discretization in time steps of fixed duration  , say

, say  , and to define the discrete time stochastic process

, and to define the discrete time stochastic process  as

as

![\[Y_{n} := \log X(nh) - \log X\big((n-1)h\big) = Y_{(n-1)h}(h)\]](https://ese3030.seas.upenn.edu/wp-content/ql-cache/quicklatex.com-877ee80fcf39b47f2b7c4e116cb57c3a_l3.png "Rendered by QuickLaTeX.com")

It follows from the GBM model, that variables are independent identically distributed normals with mean  and variance

and variance  . This is an important observation because it allows us to infer the parameters and from empirical data. Indeed, let it be available a historic sequence of stock prices

. This is an important observation because it allows us to infer the parameters and from empirical data. Indeed, let it be available a historic sequence of stock prices  for

for  , taken from a realization

, taken from a realization  of the GBM stochastic process . From we compute

of the GBM stochastic process . From we compute  to obtain a realization of the stochastic process . The drift parameter can then be estimated by the sample mean

to obtain a realization of the stochastic process . The drift parameter can then be estimated by the sample mean

![\[\hat{\mu} = \frac{1}{Nh} \sum_{n=1}^{N} y_{n} ,\]](https://ese3030.seas.upenn.edu/wp-content/ql-cache/quicklatex.com-74f8a633c8953130cfd07946ea34e67c_l3.png "Rendered by QuickLaTeX.com")

and the volatility parameter  can be estimated by the sample variance

can be estimated by the sample variance

![\[\hat{\sigma}^{2} = \frac{1}{(N-1)h} \sum_{n=1}^{N} \left(y_{n}-\hat{\mu}\right)^{2} .\]](https://ese3030.seas.upenn.edu/wp-content/ql-cache/quicklatex.com-335a8f7b0317b90acd054f6e4f552136_l3.png "Rendered by QuickLaTeX.com")

While we have given a justification for why GBM is a plausible model for stock prices, the actual motivation for their use, is that GBM models have been observed to provide reasonable fits of empirical stock price sequences. This fit is easy to observe using drift and volatility estimates  and

and  computed from empirical data. If a GBM with drift and volatility

computed from empirical data. If a GBM with drift and volatility  is a good model for the evolution of a stock price, then the variables have a probability density function (pdf)

is a good model for the evolution of a stock price, then the variables have a probability density function (pdf)  . We can then estimate the pdf of using a histogram of the

. We can then estimate the pdf of using a histogram of the  and compare it with the pdf .

and compare it with the pdf .

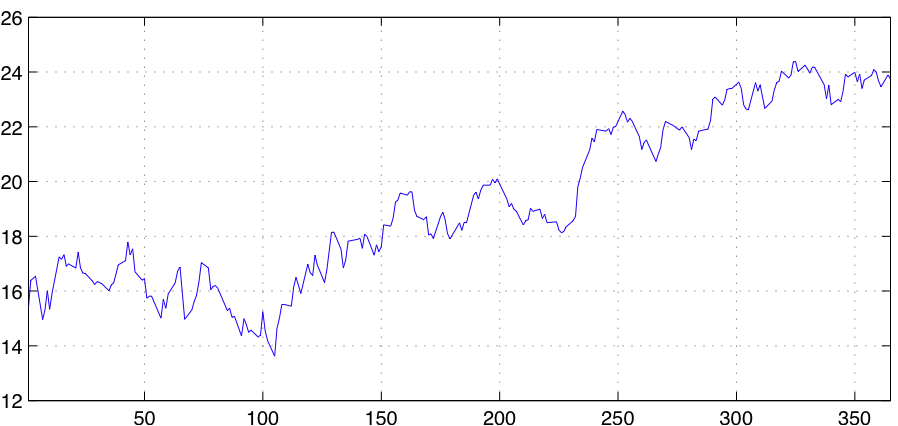

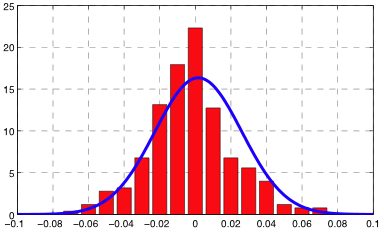

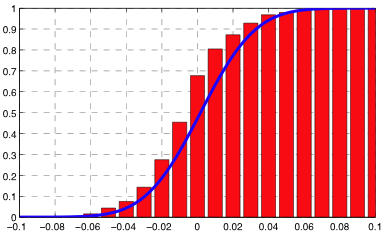

As a particular example, consider the stock price of Cisco during the year 2009 depicted in Fig. 1. More recent data for this stock and others is publicly available, see, e.g. Google finance. The comparison between the normal pdf and the histogram of is shown in Fig. 2. A comparison between the cumulative distribution function (cdf) and the empirical cdf is also shown. From either picture a reasonable fit between model and observations is seen.

Figure 2. Fit of Cisco’s stock price (CSCO) to geometric Brownian motion (GBM) model. If GBM is a good model of stock price variations, the relative changes in stock prices from closing date to closing date are independent identically distributed normal random variables. Empirical probability distribution function (left) and cumulative distribution function (right) of CSCO relative changes in closing price are compared with a normal random variable. From either picture a reasonable fit between model and observations is seen.